Fintech APIs are making it 10x faster and cheaper to bring finance products to market.

Emerging

fintech APIs makes this possible….kind of. While you’re not able to

actually start a bank in a day, you can get a consumer finance offering

to market incredibly quickly now.

Fintech APIs are making finance composable, making it 10x faster and cheaper to get consumer finance products to market.

We’re at a tipping point in finance. Your bank that you know and probably don’t love will fade into the background and consumer brands will own the last mile to the customer. These APIs are powering the revolution.

Let’s

say I want to offer a checking & savings account, credit/debit card

and a premium service to automatically invest some of your money (like Acorns).

I’ll wrap a quirky brand around it and focus my marketing on under or

poorly served segment of the market (new grads, unbanked, etc…).

Quick look at what it would have taken to do this as recently as 5 years ago:

Find

a banking partner — They’ll hold the deposits and handle the banking

compliance. There’s no list of who will do this, so start working the

phones. You’ll also have to convince them your no-name startup is an

acceptable compliance risk. This will take awhile.

Find

card partners — You’ll need a card processor, issuer and payment

network partners. You get the picture, this will take awhile also and

are individual relationships to be built and negotiated.

Build

Hairy Software — You’ll need to weave your modern software stack to use

the legacy networks these partners work on. This will be painful.

It’s going to take awhile. Be patient and spend a ton of money, you’ll get there.

Now, let’s look at how you get there today.

SynapseFi —

Set up an account and you’ve got the tools you need for your checking

and savings account as well as card issuance. Great, that was easy.

Build Modern Software — You’re building on a modern software stack. You’ll be able to deliver and iterate quickly.

OK,

this will take more than one day, but you get the point. Once you do

get to market you can quickly grow the offering and serve your customers

with new products. Want to offer stock trading? No problem, Alpaca has you covered.

Finance is shifting from the banks of the gilded age to the design thinking and A/B testing of the apps on your phone and the web.

Soon you’re more likely to deposit paychecks, get loans and credit cards from Google than Chase.

Finance is shifting from the banks of the gilded age to the design thinking and A/B testing of the apps on your phone and the web.

This massive shift is being driven by changing customer expectations, the emergence of enabling technologies and the massive reach of consumer platforms.

TL;DR

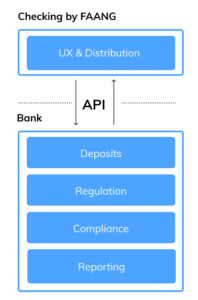

API’s are making financial products, like checking and lending, a UX and distribution problem, instead of a regulatory & compliance one.

High-engagement consumer brands like Google or Amazon can leverage these API’s and changing consumer sentiment to offer financial products directly, cutting out middlemen.

To maintain their positions, banks are in a race to build viral consumer experiences before the consumer tech giants can scale financial products. Guess who’ll win?

It’s easy to understand the attraction to financial services beyond the scale of the market size. Financial products capture huge amounts of consumer data. That data serves as the backbone of better products and UX to tech companies highly adept at leveraging personal information for profit.

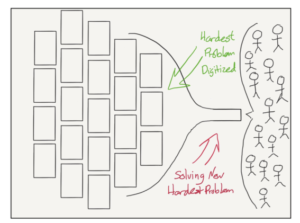

So, why now?Emerging Fintech API’s makes it easier to build products like checking and lending today. The API from a bank for deposits separates the regulatory burden (i.e. the historical barrier to entry) from the UX and customer acquisition.

APIs digitize the financial plumbing so that FAANGs can focus on what they are great at, habit forming consumer experiences.

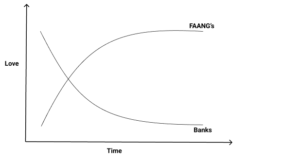

The timing is also right. 71% of millennials would rather visit the dentist than their bank. At the same time, they are increasingly trusting FAANGs with more and more of their needs.

Who Is In Control?

If banks control the underlying APIs, then it may seem like they are still in control. Which layer of the stack matters, and who’s making the money?

Banks aren’t going away, they serve a valuable purpose and will continue to make money. For now.

The last mile to the user will be served by FAANGs. Once they’ve aggregated the user demand, they will have power over the supply side (banks). Including the option of building their own banks to serve this demand.

Ben Thompson Aggregation Theory

While banks aren’t going anywhere, they are facing a future where they are cutoff from the end consumer. Ask media publishers how that’s gone for them over the last 20 years!

Banks are in a race to build high engagement consumer experiences before the FAANGs can deliver finance products to their massive and engaged userbases.

My money is on the tech giants.

Fintech 3.0

This trend has huge implications for Fintech entrepreneurs. The biggest opportunities today are in the API’s that help brands deliver financial products quickly.

The first wave of Fintech (Paypal, E-Loan…) brought traditional financial services online and created self-serve, lower cost options. It was driven by a small set of users comfortable online and happy to find a good deal.

The second wave (SoFi, RobinHood…) paired alternative data sources with novel customer acquisition tactics to deliver services more efficiently. Fees are compressing and the users were digital natives.

The third wave will see the emergence and growth of API-driven Fintech infrastructure (Alpaca, Mercury…). They’ll be integrated by consumer brands to bring finance products directly to users, removing middlemen. Fees will approach zero and the consumer experience will feel more like Instagram than Chase. The users are not only digital and mobile native, but have little to no loyalty to existing financial brands.

For example, Alpaca offers anybody an API enabling to offer users stock trading. They handle regulations and the product can focus on UX and user acquisition.

Imagine every Google Finance page connected to your Google bank and brokerage account. Google could offer one-click trading and deposits, at zero fees, subsidized by revenue earned elsewhere. They could analyze the user’s finance data to offer other finance products (robo-advisor, loans, credit cards…), but also mine the data to improve other areas of their business.

They’d have such a rich view of the user’s finance history, they could sell incredibly targeted (i.e. high cost) ad space to providers of those products interested in reaching a very specific audience. They would also be able to attribute a search ad display all the way to the purchase of an item, even if purchased offline. That’s an incredibly value feedback loop for ad buyers.

Hope you enjoyed the post, feel free to reach out with questions & comments. You can reach me on twitter!

Interview discussing the future of digitized securities and what it means for investors.

Last week I had the chance to have an in depth discussion with the folks at Crypto Gurus about Fetch, Security Tokens and Open Finance. We delve deep into the thesis that Security Tokens and Open Finance need each other to grow and prosper.

Ethereum is poised to become the enabler of a new way of fully digital finance. Just like AWS did for software backends.

Today, financial innovation is slow, costly and reserved for the few. Often it happens manually in spreadsheets and is available only for the largest of investors. Open source blockchains and digital native assets are changing this, just like AWS and open source did for software development.

Ethereum is the AWS of finance, radically transforming the cost to build and release financial products.

It used to be expensive to buy the servers and software licenses required to release software. Companies raised millions and spent much of it on Oracle licenses and server racks. Two things happened. Open source systems (bye-bye Oracle database) replaced many expensive software licenses, and AWS offered a pay-as-you-go system to replace high upfront costs. As a result, the cost to build and release a software product dropped 10x and massive experimentation blossomed.

Everybody benefits from the great software created as a result. Want an app to help meditate? Maybe find the cheapest gas station? No problem, software has you covered.

This same thing is happening in finance today. Open source systems on Ethereum are replacing the expensive and manual systems (DTCC, clearing, trustee) reducing the cost and time to bring financial products to market. We’re on the cusp of an explosion of more efficient and open financial products.

The Layers of Finance

While investors usually only pay attention to the top of the stack, what products they can access, much of the important work happens under the surface. To appreciate why we’re on the cusp of change, it’s important to understand what’s going on under the covers.

In traditional finance, layer upon layer of administrative (and very often manual) work falls to interlocking players who have not modernized significantly in decades. This creates a baseline of inefficiency and cost that restricts innovation.

Ever wonder why the minimum or cost for a financial product is so high? The reason usually lies in fixed costs or restrictions that come from an intermediary lower in the stack. Tokenized Finance upends this by replacing much of those intermediaries and fees with trustless code, it’s digital at the core. That’s critical because it’s the first step into turning finance into an API, making programmable money a possibility.

A Simple Example

Let’s take securities-based lending as an example. It’s a simple financial product, cash loans using securities as collateral, and growing quickly.

In traditional finance, brokerages and banks offer customers competitive rates with minimums ranging from $50,000 to $250,000 to access a cash loan. That’s not bad and gives investors an opportunity to take a non-purpose loan while still retaining their investment positions.

In Tokenized Finance, the financial product itself is code, protocols built on Ethereum A great example is MakerDao’s CDP which allows investors to deposit their collateral and take a cash-like (DAI) loan. It’s simple and the rates are not too different than what is available in traditional finance.

The big difference is the lack of a minimum. Code just works. It works exactly the same if the amount being deposited is worth $1 or $1M. And because there are no fixed marginal costs from intermediaries, the financial product as code can deliver the same value to the smallest and largest of investors.

Now, this may not seem like a big deal right now. Do you really want to take a $1 loan? Probably not. It does however provide a glimpse into what a future of code-driven financial products can offer.

What’s the Future?

Let’s add up what we know about Tokenized Finance.

Transforms the core of finance into API, similar to how AWS turned software infrastructure into an API.

Removes the fixed costs and antiquated rules of the financial intermediaries, removing barriers to bringing financial products to market and the costs inherent to them.

This means that software teams can now build and release financial products quickly. In addition, without fixed costs to every transaction, they can experiment with business models not before possible.

Today, that’s resulted in Tokenized Finance products that mimic traditional products with lower minimums and costs. MakerDAO for securities-based loans, Compound for money market just to name a few.

What’s more interesting is what will happen as the ecosystem grows.

Permissionless innovation with a reduced cost to bring products to market means rapid experimentation is now possible. This will create financial products not possible or conceived of in traditional finance.

Chat with team at Wyre about what a brokerage will look like in the future.

Thanks to the team at Wyre for having our me on their podcast last week. We had a great time covering a range of topics from the state of wallet software, regulation to the future of Fetch and financial services.

Emerging Fintech API’s makes it easier to build products like checking and lending today. The API from a bank for deposits separates the regulatory burden (i.e. the historical barrier to entry) from the UX and customer acquisition.

Emerging Fintech API’s makes it easier to build products like checking and lending today. The API from a bank for deposits separates the regulatory burden (i.e. the historical barrier to entry) from the UX and customer acquisition. The timing is also right.

The timing is also right.