Heavily funded Neobanks market themselves as the future of finance – mobile-first and customer obsessed. We could all use less Wells Fargo in our lives after all. However, Neobanks (Chime, N26, etc…) are not the only threat that banks should be concerned about.

Less heavily funded and heralded are autonomous finance apps (Albert, Astra, Northstar, etc…). These apps manage assets where they already reside, spread across existing accounts.

Personal finance manager apps pose a serious threat to banks by turning the deposit holding bank (Bank of America, Wells Fargo, etc…) into commodity services differentiated only by their yield or fees.

The app manages funds according to the user’s rules.

Want to save $100 each month? The app takes $100 from your direct deposit account and moves it to a high-yield savings account.

A new savings account is introduced that offers higher yield. Great, the app manages moving funds so you maximize earnings.

No single bank is motivated to offer features that work across accounts. They want all your deposits in their bank, not others. Their mission is to bundle all the finance products you need in one place and keep your business.

By removing the friction of managing funds across banks, these apps change the nature of the relationship between the user and their money. This is the threat to banks.

Gradually, the user’s attention and relationship shifts from their primary bank to this app that manages their assets. When they think about how to save, get a loan or deal with their finances they open the autonomous finance app first, not the bank’s app.

If the app manages the flow of funds across accounts, does the user care which company offers the underlying accounts? As long as it carries insurance, the criteria becomes solely the lowest fees or highest yield, not the bank brand. That’s dangerously close to accounts and the institutions that offer them becoming commodities.

I came across Alice recently and love it. It isn’t only what the product claims to do, it’s how their business model aligns so well with their users and customers.

(FYI – I’m not involved with this company in any way. I don’t know the team or invested…although I wish I was an early investor!)

First, what it does.

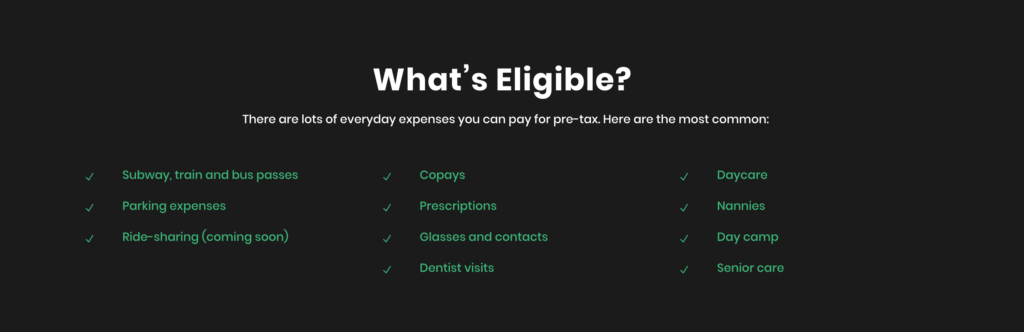

It’s an app that employees connect to their credit cards which monitors their spending. When it identifies charges eligible to be reimbursed with pre-tax w2 dollars, Alice submits the deduction to the employer’s payroll system automatically.

This is ingenious because it requires no behavior change from anybody and makes money for everybody at the same time, including Alice.

Employees – It’s simple to connect an app to your credit card and you’re more than happy to find out that bus pass you bought is now being paid for with pre-tax dollars. That’s money in your pocket.

Employers – It wires into the payroll system to automatically submit deductions. Simple. Every dollar deducted pre-tax reduces the employer’s payroll tax burden (Medicare, Social Security, etc…). That’s keeps more money in company’s bank account.

Alice – This is where incentive alignment comes in. They save the employer money and the employer pays Alice back a portion of the savings. That’s money in Alice’s bank.

The last part may seem obvious, Alice takes a cut of the savings. But consider how powerful that is when compared to a service that negotiates on a patient’s behalf to lower their medical bill. The patient received a $10k medical bill. The company negotiates it to $2k and charges the customer 5% of what they saved them, $400.

Sounds great in theory, unfortunately the patient didn’t have the $10k to start with and probably doesn’t have the $400 to pay the service provider. Even if they are relieved the bill amount was reduced, the business model isn’t fully aligned with the customer.

In Alice’s case, the employer does have the money and is happy to pay a percentage to Alice. They were going to spend it anyway! And now they get to pay less.

It’s interesting to think why this product has emerged now. What makes it possible today versus 5 years ago? A combination of things:

Fintech Infrastructure – APIs to monitoring card transactions (thanks Plaid!) have made this 10x easier.

API Economy – Of course, the payroll providers all have an API. Try having done this even 5 years ago. Remove the benefit of auto-submitting the deduction and now you have to ask the employer to do work or change their processes. Much harder sell.

Consumer Habits – That fintech infra has made services that tap into your financial accounts so much more prevalent, resulting in more apps that do so. People have gotten used to it and are more willing to try.

They may sound very different, yet are driven by the same need for the lowest possible cost of capital. The cheapest money comes from you and I depositing our cash into the bank. From there, the bank lends it out and invests it, earning revenue from the deposits.

The E-Trade numbers are particularly interesting. Trading commissions are approaching zero, a trend started by RobinHood and accelerated by Schwab. In reality though, E-Trade doesn’t make the bulk of their money from that trading fee.

They make ~18% from commissions and over 60% from net interest over deposits (from an excellent post by Charley Ma that you should read).

As Morgan Stanley offers a fuller suite of retail finance products, those deposits are the zero cost capital they can use to finance them.

As LendingClub expands their product lineup, the Radius deposits offer them the same benefit.

Would you want to be a fintech carrying capital at 3% trying to compete with others who have an almost zero cost? Easy question. With almost no bank charters being created, expect to see more and more of these deals.

How Varo’s bank charter will help prove or disprove the Neobank thesis.

Varo, a Neobank, announced this week that the FDIC approved their banking charter. This is a first for Neobanks, enabling them now to hold customer deposits and lend that money out.

You know, like a regular bank.

This will be a fascinating experiment, one that could make or break the thesis on the potential value of Neobanks.

To understand why, it’s worthwhile to explore the challenges Neobanks (Chime, Stash, etc…) face and how this charter potentially differentiates Varo.

The Problem With Neobanks

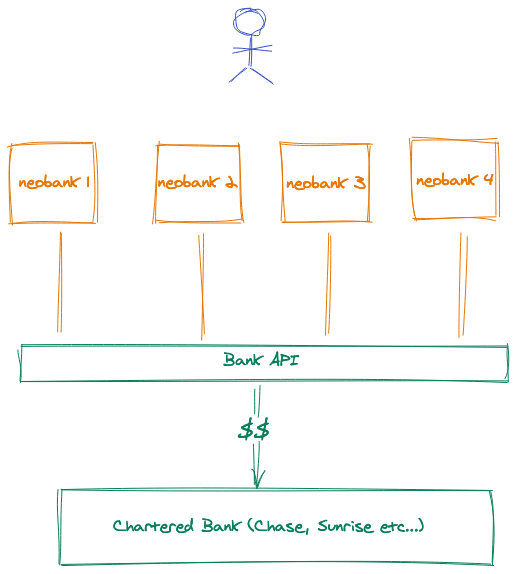

First, let’s understand what a Neobank actually is. You don’t deposit your money with a Neobank. Your money is actually held (and subsequently lent out) by a traditional bank.

It looks a little something like this.

That API between what the Neobank controls and the deposit holding bank introduces a set of challenges. It means the Neobank:

Can’t earn money by using the deposited funds to lend out at a near-zero cost of capital

Is limited in their product development by the API’s available from the underlying bank (or infrastructure provider that sits in the middle).

The bear argument for Neobanks is that they are novel UX layers and marketing channels, which can easily be replaced, to bring deposits in for the underlying bank.

On the bright side, Neobanks do not have the compliance overhead of holding customer’s money. The bull case treats Neobanks as modern finance companies with incentives aligned to their customers.

For example, Neobanks protect you from overdraft fees with warnings and quick loans because they make their money from a monthly SaaS fee as opposed to the penalty fee itself. A traditional bank has no incentive to offer the same protection, it just hurts their bottom line.

The Varo Bull Case

With their charter, Varo is betting that owning the entire stack, from UX to deposits, will enable them to:

Better anticipate, qualify, cross-sell and serve customers than banks today and at a lower cost of capital and less friction than other Neobanks.

Offer API driven banking infrastructure that others can build on (note: this one is something I’d like to see, not what they’ve publicly stated)

Can Varo do this and challenge incumbent banks in scale and market cap? Maybe.

The charter gives them a unique weapon in their arsenal. Considering it has taken them almost 3 years to get the charter issued it doesn’t appear there will be any fast followers. And with it, we’ll finally see what the value of a fully digital bank is.

Software has replaced relationship banking as the best way to acquire customers and sell new financial products.

This bodes well for the land and expand strategies of tech companies and not so well for the mythical personal relationship banks have with customers.

TL;DR

Changing customer attitudes and bank’s antiquated tech stacks are killing relationship banking, leaving banks vulnerable to competition from tech companies.

Fintechs have built modern and integrated tech stacks to better serve customer segments more economically.

Others (Uber, Shopify, etc…) are leveraging their vertical solutions to sell financial products.

Relationship Banking Test

Relationship banking posits that customers select products from banks they already use and presumably trust. And that these banks are best positioned to understand and serve their customers because of their relationship.

This just isn’t true.

Consumers, particularly younger ones, don’t discover and choose financial products based on their bank relationship. In truth:

~70% bank digitally because they don’t want to visit a branch

~50% don’t think banks are that different from one another

3x more likely to close accounts and switch than older cohorts

Let’s skip the “next generation changes everything” argument. Instead let’s use Frank Rotman’s excellent rubrik (highly encourage reading his full post for more detail).

Is it easier or more economical for current customers to access other products from you? Are you able to qualify customers because of your current relationship that others can’t?

Are you proactively suggesting and moving customers into the best products based on what you know about them?

Ever applied for a mortgage with a bank where you hold an account to find that you are filling out same information that a brand new customer would?

Ever gotten a maintenance charge on a checking account when the bank offers a free option that you also qualify for?

Then you know the answer to these questions is a resounding NO.

Banks are playing a tough hand. Their tech stacks are a mess, cobbled together over 30 years, making it difficult to serve customers across products. It also makes it expensive for them to support the niche segments that tech companies can profitably serve.

How Do Fintechs Stack Up?

Using modern tech stacks, low opex and a technology-driven mindset, fintechs focus on acquiring the best (i.e. most profitable) or underserved customers as wedge into the market. Solving one customer segment’s problem enables them to move into adjacent products and/or customer segments (‘land and expand’).

Their entire business plan is predicated on being able to answer yes to those questions. Let’s look at one of the test questions.

Is it easier or more economical for current customers to access other products from you? Are you able to qualify customers because of your current relationship that others can’t?

Remitly’s core product is an international money transfer service and many of their customers are thin file immigrants who have difficulty getting a bank account or many not have a SSN. No problem, they released a bank account that using international identification documents and no SSN to KYC a user.

How do you think these users will send money internationally from their new bank accounts? The virtuous cycle spins. It’s easy to imagine Remitly growing into loans and other products as well, all to an ignored customer segment deemed too expensive (i.e. risky) by the legacy bank tech stack.

What About “Regular” Tech Companies?

It’s not only Fintech companies the banks need to worry about.

Increasingly, tech companies that you don’t think about as finance businesses are leveraging their customer data to offer financial products more economically than a bank could. It makes sense, it’s getting easier to roll out a finance product and it’s a margin lift for their businesses.

Shopify helps anybody setup a storefront on the web and sell directly to consumers, who pay a monthly fee for the service. But, did you know that they offer loans to businesses or that this is ~50% of their revenue.

That’s a business loan, the same kind you can idealize is taken by a hopeful entrepreneur in the lobby of their local bank. Instead it’s delivered by a technology company that makes data-driven decisions based on the businesses use of their software platform.

You could imagine a Shopify competitor giving away the storefront for free to attract businesses and then earn money from loans and payment processing.

We are seeing this happening already in some verticals. Divvy is an expense management platform that is free for businesses. Completely free. They earn money from the interchange fee via use of their issued credit cards and soon through loans issued to business customers.

The permutations are endless depending on the market and pressure points. This is great for customer, not so great for banks.

Banks need a regulatory push to make our data more accessible and transportable.

Regulation could help here…gulp.

Particularly in the US, our financial data should be more easily accessible and transportable. This would make it simpler for more applications to be built to give us views into our financial life (bank account, brokerage, etc…). That in turn would allow different segments of the population to be better served for their needs. Worried about overdrafts? Remittance fees? There’s an app for that.

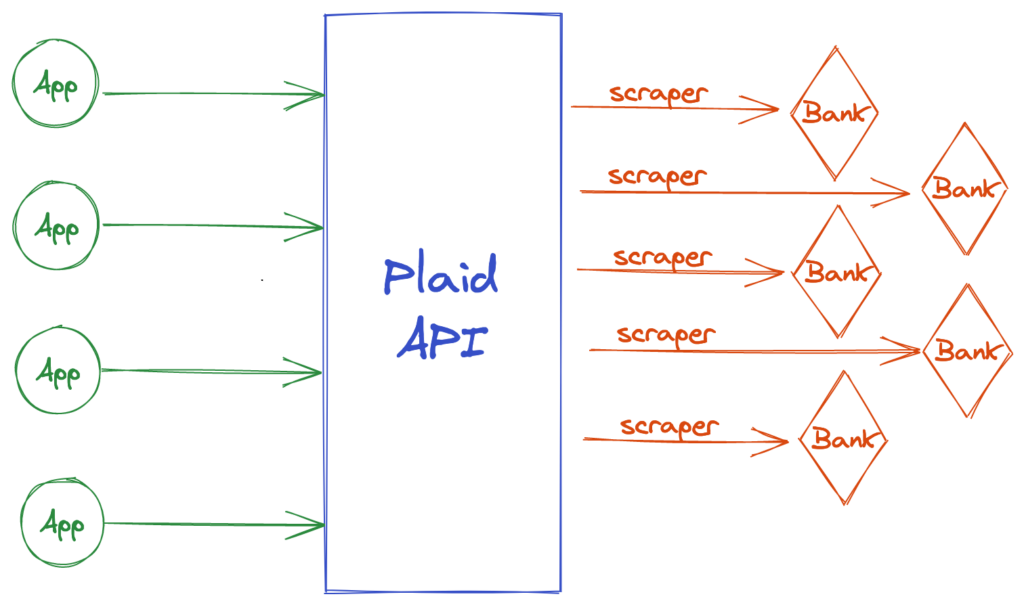

Wait. Doesn’t Plaid make financial data easy for developers to access $5.3B different ways? And didn’t Mint begin this trend over a decade ago? Yes and yes.

Notice I said improve in the title though, not enable.

First a quick background on how Plaid, Yodlee, and others work today. Primarily they compile your financial data via screen scraping. They access your account using the credentials you provide and parse the interesting data (account balance, tx dates, etc…) to share through a formal API to an app developer. For the app developer it saves time and allows them to focus on their unique business value rather than plumbing.

To be clear, I’m not condemning screen scraping. I’ve used it in multiple companies to structure data that resides in unstructured formats on websites or PDFs.

It does have serious problems though. For one, it’s brittle. The underlying site changes often and when it does your scraper breaks. So access to some banks is constantly under repair and there is no way to know when. Also, it can break completely when the provider of the website wants to break your scraper. And they have multiple reasons to want to do this.

So what can be done? Why don’t banks adhere to a standard format of making data available? It is your data in the first place. Unfortunately, they have no motivation to do so. They prefer you live within their universe of products and not easily manage finances across banks or have simple access to products elsewhere that would compress their margins.

Europe offers a roadmap to solve this with their PSD2 initiative. Among others things, PSD2 requires banks to adhere to a standard API for data access. Unfortunately, there probably isn’t another way to make this happen among banks that aren’t motivated to do it on their own. More unfortunately, we probably won’t see a similar rule in the US.

This wouldn’t negate the value of Plaid and similar services (see Tink for proof). It would serve to make their APIs more robust and reliable. The winners would be end users benefiting from more ways to manage their financial health. And we should all want that outcome.

Plaid’s acquisition is a tailwind for the next wave of fintech infrastructure networks.

Big news, $5.3B big. Everybody has takes, including Visa themselves, on why fintech infrastructure is more important than DTC fintech. We’re all geniuses in hindsight.

Unsurprisingly, Ben Thompson has one of the best explanations of the rationale [paywall]. It ties back to the power of a network that can not only provide read-only access to your money, which is what Plaid offers. The future is programmatic read and write access.

Visa today sits in the middle of a 3 sided network.

Merchants – who offer products and benefit from a network that extends credit and fixed payment terms

Consumers – who need credit and convenience

Banks – who have money to extend credit

Plaid today sits in the middle of a read-only 3 sided network, a threat and opportunity to Visa’s business

Consumers – who want modern access to their finances

Banks – where money resides and earns interest, is lent/borrowed/etc…

More importantly, though, is the power of inertia: as long as it is hard to move money around, the more likely it is that that money will stay in the bank, collecting minuscule interest; or, if customers need value-added services, the path of lowest resistance will be simply getting them from their bank.

An API-based world could change this dramatically: suddenly consumers could commission robo-advisors to move their cash to whoever is offering the best rates, or to automatically refinance debt. Value-added services from multiple vendors would be equally easy to access, meaning they would have to compete on price or terms. In other words, much like the open Internet, banks fear that profits will be rapidly transformed into consumer benefit.

Ben Thompson

Plaid’s founders, team and investors are huge winners obviously. The secondary effect is the rising tide this will provide to the next wave of fintech infrastructure players like Astra, Alpaca & SynapseFi.

If you’re building a bank today, you’re in luck. Much of what you need is available via API so you can skip the months of legwork to find bespoke banking and compliance partners.

If you’re building a bank

today, you’re in luck. Much of what you need is available via API so

you can skip the months of legwork to find bespoke banking and

compliance partners.

You can start building on day 1.

Here’s a few of the things you can start building quickly by standing on the shoulders of g̵i̵a̵n̵t̵s giants-in-the-making.

KYC/AML

To

offer most financial products you’ll kneed to abide by Know Your

Customer (KYC) and Anti Money Laundering (AML) rules. This will involve

asking the user for personal and financial information and verifying

it’s authenticity. These providers automate much of the work required to

verify the information collected.

ID Verification — Is that picture of their passport or driver’s license they uploaded authentic and actually of them? Trulioo and Jumio will handle that check for both USA and international applicants.

Accuracy

& Watchlist Scans — Is the address they provided really theirs? Is

their legal status free of flags for money laundering or international

watchlists? Blockscore handles those checks via its API.

Account Inspection

While

onboarding the customer, you’ll often want to confirm and connect with

financial accounts they own. Perhaps you’ll want to confirm balances or

offer to ACH funds into their new accounts.

Want

to offer a checking account? Skip searching for a banking partner to

hold the funds and allow you to onboard customers. These APIs enable you

to skip the partnership and plumbing legwork.

Perhaps you’ve got a spin on the traditional credit card and think you can get into the flow of interchange fees. Maybe a card for teens or one to control your spending?Avoid the upfront fees and convincing card issuing partners and use one of these APIs instead.

Now

that you’ve got millions of people direct depositing their paychecks

and spending using your credit card, let’s offer them some investment

tools to put their money to work. Sure, they could open an E-Trade

account, but wouldn’t it be easier to do this in the same account they

already use for their personal finances? You could start the

multi-month, multi hundred thousand dollar process to launch a

Broker-Dealer, or leverage one these APIs to get started immediate.

These APIs are serving as the infrastructure anybody needs to get finance products to market quickly. The end result will be more products tailored to more market segments and hopefully better finance experiences and outcomes for all of us.

Apps automating personal finance will improve financial health and relegate bank accounts to commodities offering highest yield and lowest fees.

Banks wage an ongoing war to hold your money. You’ve seen the tactics — higher interest rates and free credit reports are the modern free toaster to open a new account and setup direct deposit.

You get those free toasters because:

Banks earn money by holding your money.

There’s inertia to deposited money. You’re too busy to move it around optimally, it generally stays where deposited. The bank that gets it first gets to keep making money from it.

In the perfect world, your money would flow from paychecks to where it’s needed at just the right moment. It would earn you the highest return in the right accounts for the right purpose, while ensuring your bills and payments are covered.

A new generation of apps are changing money management by automating personal finance. These apps will become the primary way people manage their money, owning the customer relationship and ultimately their deposits.

Autonomous Finance apps that improves financial health and save time are the new battleground in finance.

Personal Finance Today

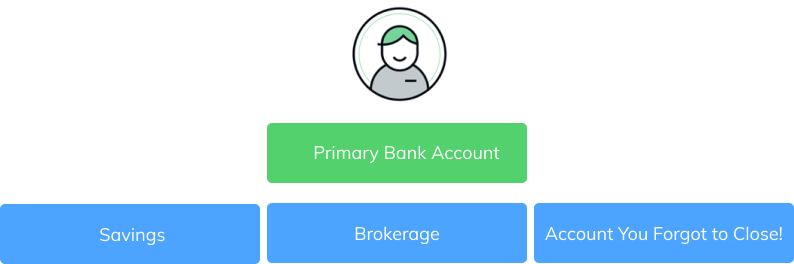

Today, your finances probably look something like this.

Your income flows into a main account and perhaps you move some for savings and bills elsewhere. If you’re like most people, you probably don’t do that, just operating out of that one account.

Banks battle to be that primary account.

Maybe there are higher yielding accounts elsewhere? Maybe you should be moving set amounts every month for savings? Maybe you’ve exceeded the SIPC insurance limit and really should split money into separate accounts so you’re protected from a black swan? Maybe you’re forgetting to move funds some months and accruing overdraft fees?

People are busy and distracted. So maybe they do none of these things even though it’s in their best interest.

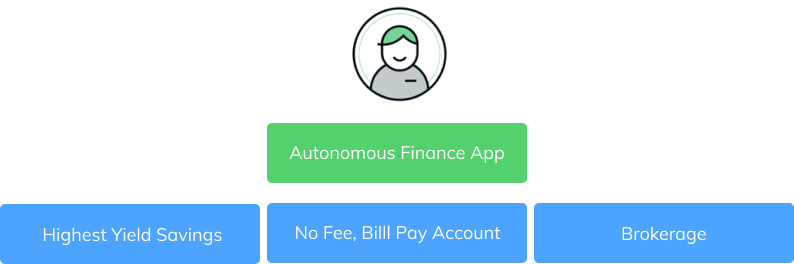

How Autonomous Finance Apps Change Things

Tomorrow, Autonomous Finance apps will be the primary way you manage your money.

The application manages the movement of funds according to rules you set or that it figures out based on your behavior.

Need $1,000 in your checking account on the 5th of the month? No problem, the app will make it happen and ensure you don’t get hit with an overdraft fee.

Want to put aside $100 each month for a large purchase? Done.

A new savings account is introduced that offers higher yield? Easy, the app manages moving funds so you maximize earnings.

The key thing here is that your primary relationship is with the application. The accounts used become commodities that can be interchanged by you or the app itself. Accounts compete purely on their utility for the purpose they serve—interest rate, fees, etc…

Owning the customer will take more than getting them to open an account and setup direct deposit. The software eats the inertia of how accounts are used. Owning that software and providing the user the best experience is the new battleground.

Ultimately, only one or two of these businesses are likely to emerge as large, standalone players. We’ll all benefit from how they will rewire the competitive landscape by having more options to manage our money more easily and efficiently.